If You Knew the Headlines in Advance, Would You Have Picked the Winner ?

A thought experiment on why even perfect foresight about the news is not enough, and why owning the market usually is.

Imagine it is the end of 1999. The millennium is about to turn, the dot-com boom is at full roar, and someone hands you tomorrow's newspapers for the next 25 years. Not the share prices, just the headlines. You flick through and two pharmaceutical stories jump out.

The first is a dream. Pfizer has just launched Viagra, one of the most famous drugs ever brought to market, and there is far more to come. In 2000, the company pulled off a hostile takeover of Warner-Lambert to get sole ownership of Lipitor (a cholesterol-lowering medication), which went on to become the best-selling prescription drug in history. In 2009, Pfizer bought Wyeth which turned it into a vaccine powerhouse. And then, in 2020, the papers tell you, a global pandemic will shut down the world. Pubs closed. Airports empty. Offices deserted. And the company that rides to the rescue will be Pfizer, delivering the first authorised Covid vaccine in the West. It will not just be a successful product. It will be, for a period, effectively compulsory. You will need proof of a Pfizer jab, or one of its rivals, to go for a pint, to eat indoors, to board a flight, to go on your holidays. Governments will queue up to buy it by the hundreds of millions of doses. Revenue from the vaccine and the related antiviral will exceed fifty billion dollars in a single year. It is hard to imagine a more perfect headline for a shareholder: the whole world, mandated by law, to buy your product.

The second story is a nightmare. Johnson & Johnson will spend much of the same period engulfed in claims that its talc products were linked to cancer. Tens of thousands of lawsuits. Multibillion-dollar jury verdicts. Investigative journalism, regulatory scrutiny, and repeated attempts to resolve the litigation through settlement proposals running to many billions of dollars.

Armed with those headlines, which company would you have backed with your savings?

Most people would take Pfizer without hesitation. And most people would have picked the wrong one.

What actually happened

Starting the clock at the end of 1999, just before the dot-com crash, here is how the following 25 years played out.

Pfizer traded at $46 a share at the turn of the millennium, having peaked at around $50 during 1999 (split adjusted). It ended 2024 at roughly $26.50. Excluding dividends, the share price fell by circa 50 per cent from its peak, over a period in which the company launched Viagra's successors, completed enormous acquisitions and delivered the most commercially successful vaccine launch in history. Dividends softened the blow, but even including them, an investor's total return worked out at only around 2.50% per cent per annum.

Johnson & Johnson, the company with the toxic headlines, compounded at roughly 7.5 per cent per annum including dividends over the same 25 years, several times the outcome of the Pfizer investor. It raised its dividend every single year throughout the litigation, a streak now stretching beyond six decades. The company the headlines told you to avoid quietly multiplied its shareholders' money many times over.

And the third option, the boring one? The S&P 500, of which both companies are members, delivered an annualised total return of just under 8 per cent per annum with dividends reinvested. No drug pipelines to analyse, no litigation risk to weigh, no headlines to interpret. Just ownership of the whole market, including both Pfizer and Johnson & Johnson, the winners and the losers, at a cost of a few basis points a year. The index investor beat the Pfizer investor by a country mile and finished shoulder to shoulder with the J&J investor, without ever having to choose.

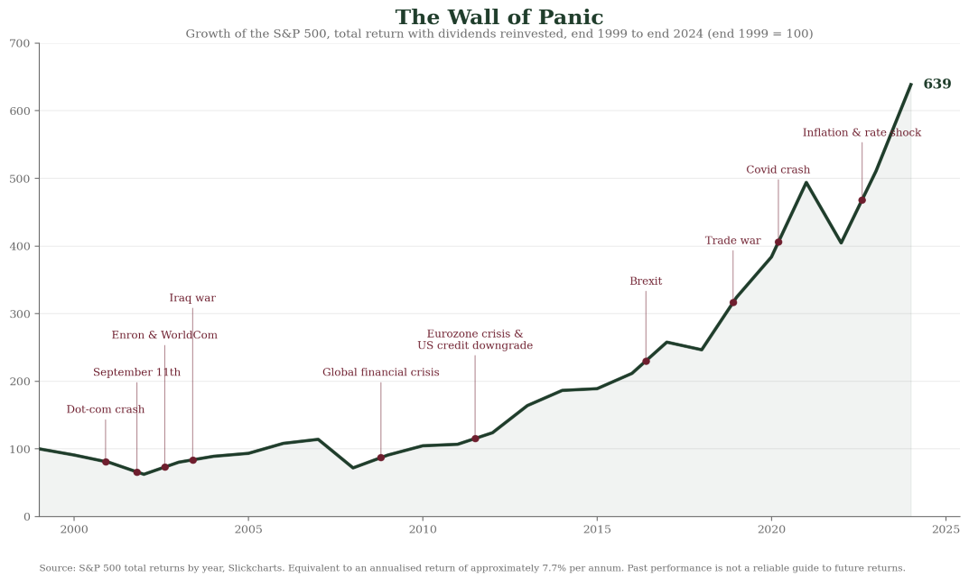

The wall of panic

That return was not earned in calm seas. It is worth pausing on what the index investor had to sit through to collect it:

- The dot-com crash, which roughly halved the market between 2000 and 2002

- September 11th

- Enron and WorldCom

- The Iraq war

- The global financial crisis of 2008 and 2009, when the index fell by more than half and respected voices questioned whether the banking system itself would survive

- The eurozone crisis and the downgrade of America's credit rating

- Brexit

- A trade war

- The fastest crash in stock market history in the spring of 2020, when Covid arrived and markets fell by a third in a matter of weeks

- The inflation and interest rate shock of 2022

Twenty-five years of headlines screaming that this time was different, and an investor who ignored every single one of them compounded at close to 8 per cent per annum. The market did not deliver that return in spite of the panics. Enduring the panics is precisely what investors are paid for.

A good company is not the same as a good investment

The lesson here is subtle, and it is not that news does not matter. It is that a good company and a good investment are two different things. What determines your return is not how good the business or its products turn out to be, but how good they turn out to be relative to what was already priced in when you bought.

By the end of 1999, Pfizer was one of the most admired companies in the world and its valuation reflected decades of expected brilliance. The company continued to be brilliant. It saved lives on an extraordinary scale. But it was still a poor investment, because the starting price left no room for the ordinary realities of the pharmaceutical business: patent cliffs, failed trials, and revenue that must be rebuilt from scratch every decade. Even the Covid windfall, tens of billions of dollars of mandated demand, proved temporary, and the market knew it.

Johnson & Johnson was the mirror image. The market stared at the litigation headlines, priced in an enormous amount of bad news, and the underlying business of medicines and medical devices simply kept compounding underneath. Talc was the headline; it was never the whole company.

The share price is not a poll of how good the news is. It is an auction between millions of investors about how good the news is relative to what everyone already expected. That is why knowing the story in advance, even perfectly, is not the same as knowing the return.

Even the professionals cannot do it

If picking stocks were merely difficult, one would expect professional fund managers, with their analysts, models and access to management, to manage it reliably. The evidence says otherwise.

Dimensional Fund Advisors, in its long-running study of the US fund industry, examined thousands of equity funds over rolling twenty-year periods. In its analysis of funds available at the start of 2006, more than half did not even survive the following two decades, and only around 12 per cent both survived and outperformed their benchmark. Broader versions of the study covering periods through 2023 put the figure at roughly 18 per cent. Call it somewhere between one in five and one in eight. And identifying those winners in advance is another matter entirely, because the same research finds that past performance tells you almost nothing: of funds that ranked in the top quartile over one five-year period, only around one in five repeated the feat in the next.

These are professionals. They do this all day, every day, with resources no private investor can match. Roughly four out of five of them, over a twenty-year horizon, would have been better off buying the index.

The Biograph view

Our thought experiment loaded the dice in favour of stock picking. We gave the investor the headlines in advance, something no real investor will ever have, including the single most investable-sounding headline imaginable: a product the entire world would be required to buy. The intuitive choice still lost badly, both to the unloved alternative and to the index.

The practical conclusion is liberating rather than defeatist. You do not need to out-analyse the pharmaceutical industry, forecast litigation outcomes or beat the smartest traders in the world to earn an excellent long-term return. You need to own the market, keep your costs low, stay diversified across the Pfizers and the Johnson & Johnsons alike, and let 25 years of compounding do the work, through every crash and crisis along the way. A return of close to 8 per cent per annum, achieved by doing almost nothing, turns out to be a result that the overwhelming majority of professional investors fail to match.

The hardest part is not the analysis. It is the patience.

And one final footnote. As at the end of June 2026, Pfizer's share price stood at $24.08. More than a quarter of a century on from its dot-com era peak, it still has not recovered.

Warning: The value of your investment may go down as well as up |

Warning: Past performance is not a reliable guide to future performance |

Warning: The above is general in nature and any specific action should be discussed with your Financial Advisor |